Bahrain Education sector VAT treatment guide

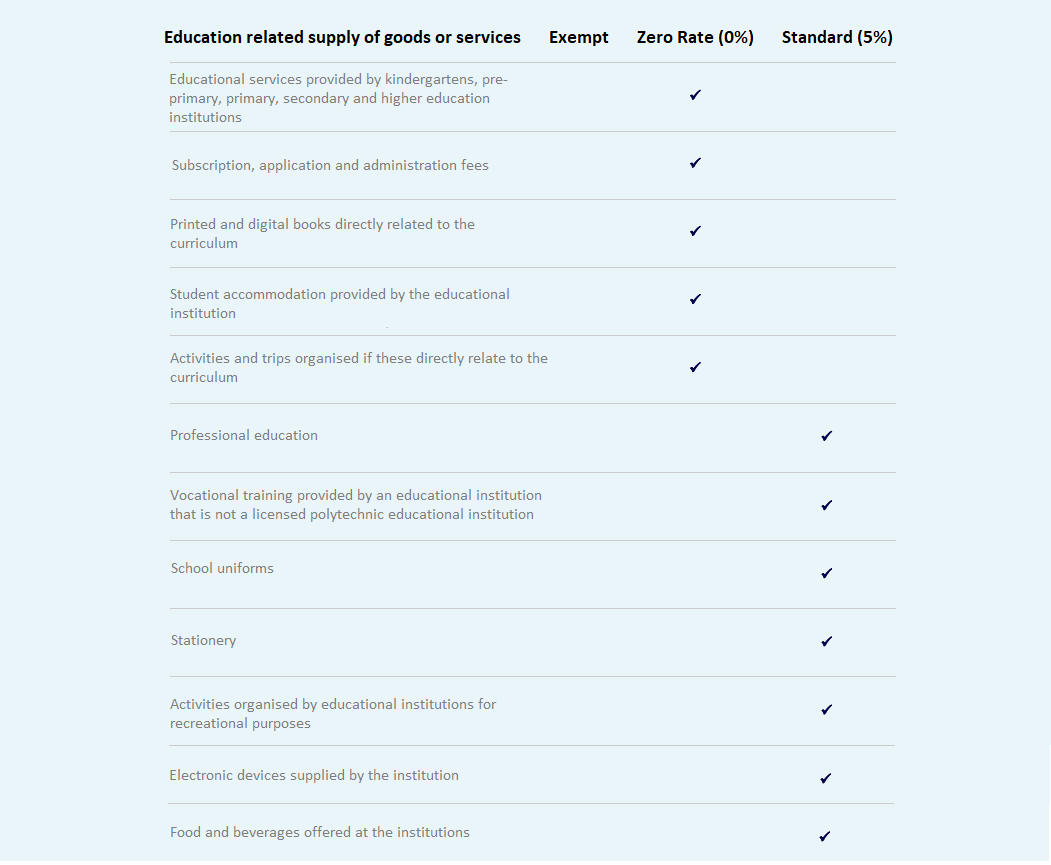

VAT on Education related activities are zero or standard rated.

Education service as defined by Bahrain VAT law:

The educational institutions must be licensed by a competent authority in the Kingdom and the educational services must be provided to a student who is enrolled in that school or institution.The supply of educational services and related goods and services by kindergartens, pre-primary education, primary, secondary and higher education institutions are subject to VAT at the zero-rate.

Professional education and vocational training (unless the vocational training is provided by a polytechnic educational institution licensed by the relevant authority in Bahrain) does not qualify as educational services for the purpose of applying the zero-rate. These services are therefore subject to VAT at the standard VAT rate of 5%.

For easy understanding of VAT treatment in Bahrain for education sector, we have listed education related supplies by VAT rate. Check this full list.

Zero-rated education related goods and services:

Below are some examples of “associated goods and services” qualifying for the zero-rate when provided by qualifying educational institutions:• Subscription fees, application fees or any form of administration fee

• Printed and digital books and reading material which are educational in nature and are directly related to the curriculum

• Student accommodation supplied by the educational institution to students enrolled with the educational institution provided that such accommodation has been constructed or adapted specifically for use by students

• Activities and trips organized by the educational institution for its students if these form part of the curriculum and are not predominantly recreational in nature

Standard-rated education related goods and services:

On the other hand, the following supplies do not qualify for the application of the zero rate:• The provision of school uniforms

• Food and beverages supplied at the educational institution

• Stationery

• Electronic devices supplied by the educational institution

• Activities and trips organized by the educational institution for recreational purposes