Bahrain Financial Services VAT treatment guide

Below is list of Financial Services and associated VAT

Financial Services as defined by Bahrain VAT law:

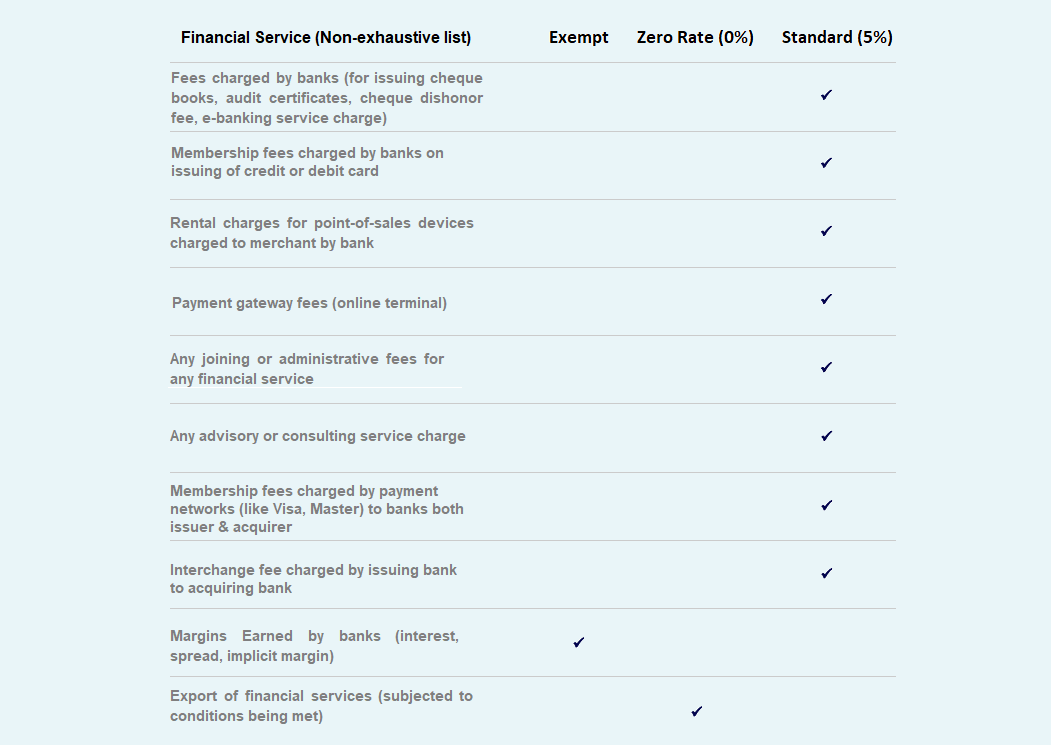

Financial services are services that directly relate to money, financing, debts and other financial securities as well as fund management.Most of the time, suppliers in the financial services sector will perform both VAT taxable and VAT exempt supplies and most of their expenses will be used in the making of both taxable and exempt supplies. As a result, the supplier will only be able to partially recover the VAT charged on these expenses. Please note, only if the financial service is exported and export of service conditions are met then the zero-rate VAT shall apply.

Here is the categorization of non-exhaustive list of financial services for VAT purpose.

1. Money related Services:

Services typically performed by banks or similar organisations in connection with the operation of current, deposit or savings accounts. Example: Issue of credit card, cheque book, Convenience services, interchange services.2. Credit and financing services:

Lending or advancing money to customers in consideration for interest payments. Example: Granting of secured and non-secured loans.3. Debts and debts related services:

Transactions dealing with debts and their recovery. Example: Debt collection, securitization.4. Capital and money market:

Issue, allotment, renewal, amendment, rent or transfer of ownership of a debt or equity security (whether listed or unlisted). Example: Issue and sale of shares, bonds. Underwriting services5. Financial derivatives:

Supply or issue of financial derivatives or deferred contracts or any necessary arrangements for them. Example: Supply of forwards, futures, options6. Asset management:

Investment management services (i.e., direction of a client's cash and securities by a financial services company). Example: Discretionary asset management. Investment advisory services7. Islamic Finance products:

Islamic finance products provided in accordance with legally approved contracts, which are similar to conventional financial products in terms of the intended objective and materially achieve the same result. Example: Commodity Murabaha / Tawarruq, Ijarah / Ijarah followed by a sale.8. Insurance and life reinsurance:

Provision or transfer of ownership of a life insurance or reinsurance contract. Example: Provision of life insurance / reinsurance cover or life Takaful / re-TakafulFor VAT purposes, it is not required that the business is specifically regulated by Central Bank of Bahrain for its services to be regarded as “financial services”.

The “financial” nature of a service from a VAT perspective, is linked to the features of the service itself, as opposed to the regulatory status of its supplier. The provision of “financial services” for VAT purposes is therefore not reserved to banks or other regulated financial businesses. For instance, the provision of an interest-bearing loan is a financial service for VAT purposes whether the loan is made by a regulated bank or by any other taxable person.