Bahrain Real Estate VAT treatment guide

VAT on Real estate related activities are zero or standard rated.

Real estate as defined by Bahrain VAT law:

For VAT treatment the real estate, as per the executive regulation, is defined as services that include accommodation services, services related to construction, services by real estate experts, estate agents, auctioneers, architects, engineers and others who perform tasks and work related to real estate.These services must be directly connected to specific real estate. In this regard, real estate is defined as any of the following:

• An area of land over which rights or interests can be created

• A building, structure or engineering work permanently attached to the land

• A fixture or equipment which makes up a permanent part of the land or is permanently attached to a building, a structure or engineering works

Real estate does not include any furniture, fittings, plant and apparatus which are not attached to land or a building and which can be removed without damaging the property. Where residential accommodation is provided in the form of furnished or semi-furnished accommodation, the entire consideration will be considered as a supply of real estate, unless a separate charge for the furniture is made. However, it is important to consider whether the accommodation will meet the conditions for serviced accommodation as a different VAT treatment will apply.

VAT Treatment on supply of real estate:

The sale, lease or license of real estate located in Bahrain is an exempt supply, regardless of whether the real estate is residential, commercial or land (bare or partly developed). Some supplies will not be considered as real estate for VAT purposes (as described below in section 4.3) and the VAT implications of these supplies will need to be determined on a case by case basis. VAT incurred on expenses or purchases (i.e., professional legal fees, refurbishment, etc.) that is attributable to making exempt supplies of real estate will not be recoverable by the taxable person. Businesses that only make exempt supplies for VAT purposes and which do not receive taxable supplies of goods or services for which they are liable to account for VAT at 5% under the reverse-charge mechanism will not be able to register for VAT.Services not considered as supply of real estate:

The following supplies will not be considered as the sale or rental of real estate and will therefore be taxable at the standard rate of 5%:a. Hotel accommodation and related services

b. The provision of paid car parking for periods of less than one month

c. The provision of serviced office space where the customer does not have the right to use a designated space on an exclusive basis

d. Rental of a function room, hall or similar facility

e. Management services, utilities, telecommunications, internet and television charged for separately and in addition to the rent

f. Providing permission to affix equipment and signage to land or buildings.

For easy understanding of VAT treatment we have listed real estate related activities by VAT rate:

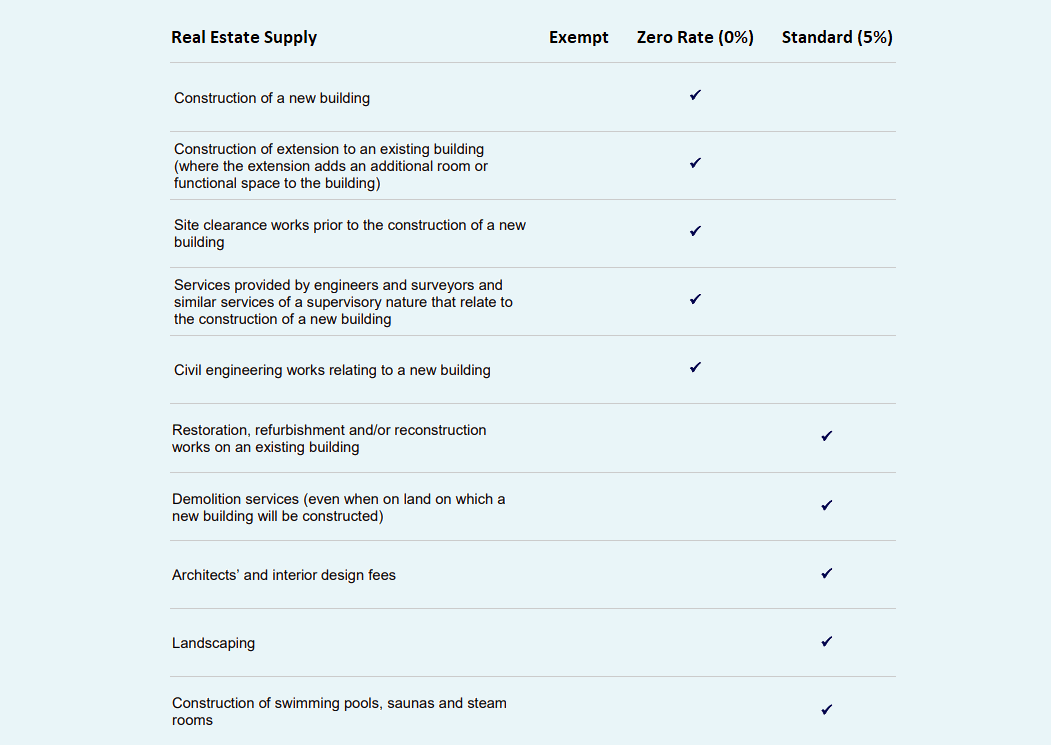

Zero rated real estate supplies:

1. Construction of a new building2. Construction of extension to an existing building (where the extension adds an additional room or functional space to the building)

3. Site clearance works prior to the construction of a new building

4. Services provided by engineers and surveyors and similar services of a supervisory nature that relate to the construction of a new building

5. Civil engineering works relating to a new building

Standard rated (5%) real estate supplies:

1. Restoration, refurbishment and/or reconstruction works on an existing building2. Demolition services (even when on land on which a new building will be constructed)

3. Architects' and interior design fees

4. Landscaping

5. Construction of swimming pools, saunas and steam rooms