Introduction:

Bahrain introduced VAT on 1 January 2019. This article summarizes the general principles of Value Added Tax (VAT) in the Kingdom of Bahrain. It provides an overview of the VAT rules and procedures in Bahrain and outlines basics to comply with the Bahrain VAT law.

What is Value Added Tax in Bahrain?

As explained by the VAT general guide shared by National Bureau for Revenue of Bahrain, VAT is an indirect tax on consumer spending. It is collected on supplies of goods and services as well as on imports of goods and services into Bahrain. As per the VAT law, VAT applies at 5% if a supply of goods and services is made:

• By a taxable person

• In Bahrain

• The supply is not specifically exempted from VAT or subject to the zero-rate.

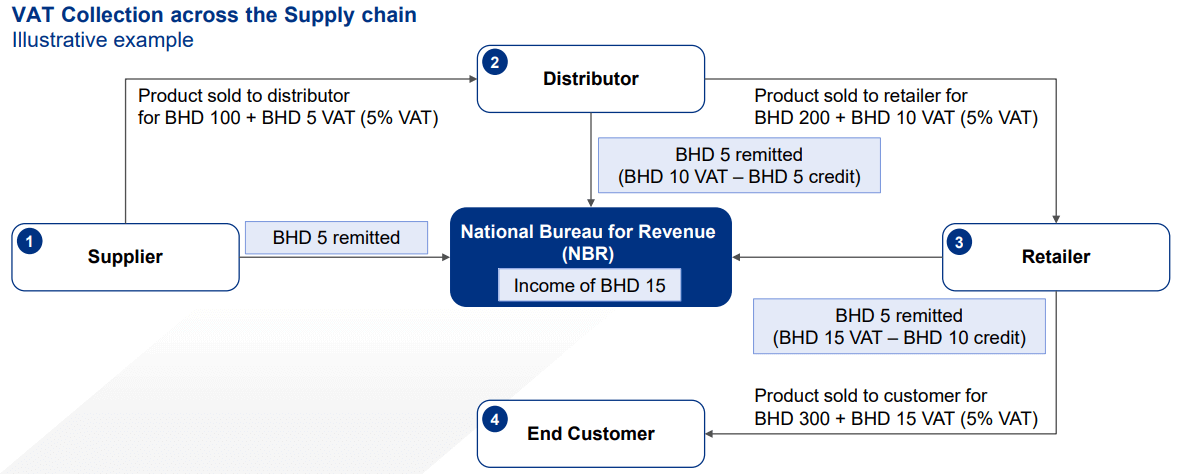

VAT is collected at every stage of the supply chain, eventually the end consumers of goods and services bears the cost as VAT is a tax on consumption. The image below clearly explains the VAT collection across the supply chain:

Who is a taxable person?

As per the definition provided by documents published by NBR, “a taxable person is a person carrying out an Economic Activity independently for the purposes of generating income and who is registered or obliged to register for Tax purposes in accordance with the provisions of this Law.”

Please assess yourself based on the criteria below to determine if you are a taxable person:

a. You are a person:

The VAT Law defines a person as any natural or legal person, whether public or private, or any other form of a partnership. Examples of “person” include individual traders (establishments), companies (whether private or public), partnerships, charities and government bodies. In addition, it includes individual professionals such as doctors, lawyers, architects, etc.

b. You carry out an economic activity:

Which is independently for the purpose of generating income An economic activity is an activity that is conducted in an ongoing and regular manner for the purpose of generating income, and includes commercial, industrial, agricultural or professional activities or services or any use of tangible or intangible assets, and any other similar activity.

Please note, a one-off transaction is not an economic activity. Further, it is not necessary that the activity is profitable for it to be an economic activity. It is enough if the activity is conducted for the purposes of generating income. Only taxable persons are authorized to charge VAT on their supplies. It is therefore critical for you to determine whether you are a taxable person before you start charging VAT on your supplies.

Who should register for VAT?

When you are resident in Bahrain and meet the criteria to qualify as a taxable person, you are required to register for VAT if:

The amount of your annual supplies during the previous 12 months exceeds the threshold of BHD 37,500;

The amount of your annual supplies to be provided in the next 12 months is expected to exceed the threshold of BHD 37,500.

Please note, the above criteria is applicable only from 1 Jan 2020. As VAT is getting implemented in phases please check the below infographic to check the timeline for mandatory and voluntary VAT registration thresholds and timelines.

How to register for VAT?

Follow the below five steps to register for VAT:

1. Create a NBR profile

2. Populate the NBR form and specify your information – which can be accessed using the following link: https://www.nbr.gov.bh/form.

Required information includes:

– Taxpayer details (legal name, legal form, address, contact details, VAT eligibility date, etc.)

– Commercial registration details (CR Number, CR date, subsidiary details, sector, etc.)

– Financial information (annual value of supplies, expenses, imports and exports)

– Registrant details (name, identification number, DOB, job title, etc.)

3. Submit your profile creation request. You should be receiving an e-mail from NBR confirming that your application was received and being processed.

4. If your NBR profile is approved, you will be provided with login details to access the registration form.

5. Complete the registration form in a “single click” – which can be accessed using the following link: https://www.nbr.gov.bh/login.

When the NBR processes and completes your registration, you will receive a VAT registration certificate confirming your registration and your VAT account number (also referred to as your Tax Registration Number (TRN)). This certificate must be placed in a visible spot of your establishment(s). Here is how the certificate will look like:

What are the consequences of failing to register for VAT?

If you are required to register for VAT, but have not done so by the relevant deadline, the NBR may automatically register you from the date on which you should have been registered. You will be required to account for all the VAT due on your supplies and purchases of goods and services since your effective date of registration. If you do not register 60 days after the registration period completion, the NBR may apply administrative penalties of up to BHD 10,000 as well as sanctions in case of offence qualifying as tax evasion as per section 14 of this Guide.

What transaction are covered under VAT?

If you are a taxable person, you need to consider whether the transactions you are making fall within the scope of VAT as this will be the first step before deciding whether VAT in Bahrain is applicable on such transactions. If a transaction is not an “in-scope” transaction, it is considered as being “outside the scope of VAT” and is disregarded for VAT purposes. If a transaction is an “in-scope” transaction, you will have to assess whether VAT in Bahrain is applicable and at which rate.

The VAT Law defines four categories of transactions falling within the scope of VAT:

• Supplies of goods by a taxable person

• Supplies of services by a taxable person

• Imports of goods

• Deemed supplies by a taxable person

Only those transactions falling within one of these four categories are considered in the scope of VAT.

Transactions outside the scope of VAT

The below are examples (non-exhaustive) of transactions that do not fall within the scope of VAT:

• Tips paid on top of a bill, where the customer tips due to his own independent choice

• Penalties for late payment or infringement of the law. Such transactions are not consideration for a supply, but merely punitive in nature

• Goods that are returned (e.g., deficient or unsatisfactory). The customer does not supply the goods to its supplier, the return is a reversal of the initial supply

• The receipt of an inheritance through a will

• The replacement of goods under a warranty. The replacement goods are not seen as being separately supplied to the customer, provided the replacement is covered under the warranty

• Receipt of an indemnity payment as part of an insurance contract or in the context of litigation. Such payments are not consideration for a supply of goods or services made by the insured person or by the party to the litigation as they are paid to compensate loss or damage

• The receipt of dividends. This is because the exercise of shareholder rights is generally not considered as an economic activity for VAT purposes

Place of supply rules

For Bahrain VAT Law to apply and for Bahrain VAT to be charged, a transaction must fall within the VAT jurisdiction or “territorial scope” of Bahrain. It is therefore critical to know where a transaction takes place or is deemed to take place for VAT purposes.

Place of supply definition differs for goods and services.

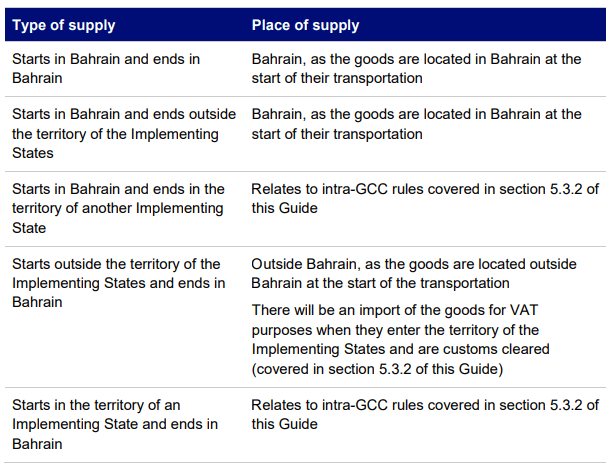

For supplies of goods

The general place of supply rules for goods will depend on factors including whether the supply includes a transport of the goods or their installation. For goods supplied without transportation and without installation, the place of supply is where the goods are placed at the disposal of the customer.

For goods supplied with transportation, the place of supply is where the transport starts. This applies whether the transport is carried out by the seller, the purchaser or a third party on their behalf.

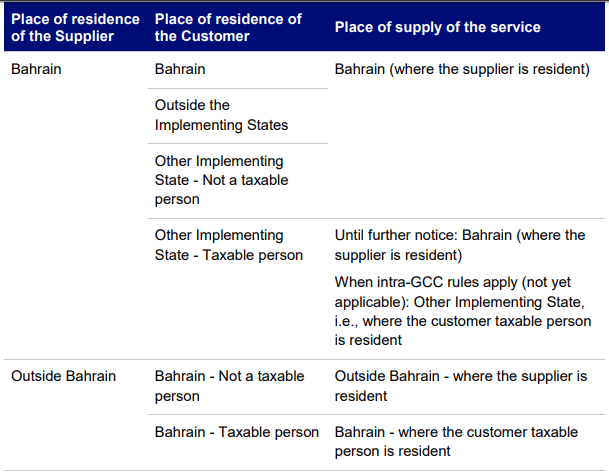

For supplies of services

There are two general place of supply rules for services. These are based on the place of residence of either the supplier or the customer. (See Appendix B for information on what constitutes a place of residence.) The key differentiator between these two rules is the VAT status of the customer, i.e., whether it is a taxable person or not.

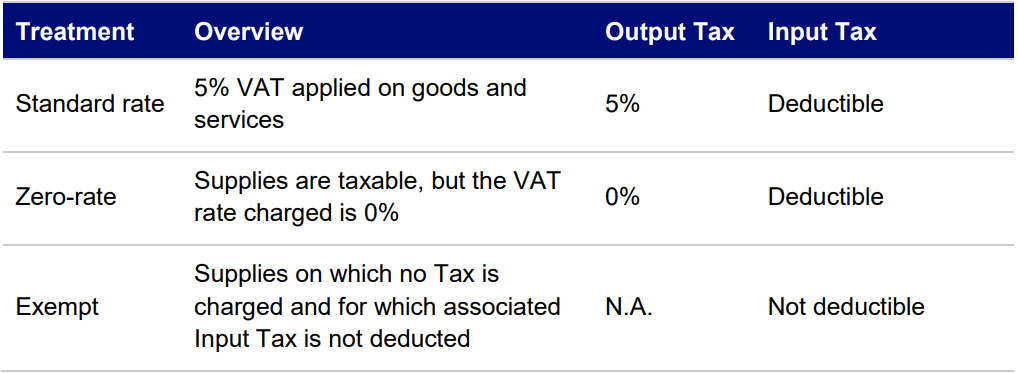

VAT treatment in Bahrain

A supply of goods or services taking place in Bahrain for VAT purposes can be subject to VAT at the standard rate of 5% or at the rate of 0% unless it falls within the scope of a VAT exemption.

This section provides an overview of the VAT treatment applicable to supplies of goods and services as well as imports of goods happening in Bahrain. If you are a taxable person, it will help you identify the correct VAT treatment applicable to your transactions in Bahrain.

Disclaimer: This Guide is intended to provide general information only, and contains information based on document released by National Bureau for Revenue (NBR) on its portal and all the images are sourced from the same document. No responsibility is assumed for the VAT laws, rules or regulations in the Kingdom of Bahrain. This Guide is not a legally binding document, please refer to the complete policy document on Bahrain VAT law, released by the authorities. This document should be used as a guideline only and is not a substitute for obtaining competent legal advice from a qualified professional.